UK Stock Market Forecasting

The Problem

The stock market is notoriously volatile and difficult to predict due to the high noise and non-linearity of financial data. Traditional statistical models often fail to capture the complex temporal dependencies and the "regime shifts" caused by external market sentiment.

The Solution: Multi-Model Architecture

I developed a robust machine learning pipeline that integrates technical indicators with alternative data (sentiment analysis) to predict the FTSE-100 index. The system utilizes multiple deep learning architectures to capture different facets of market behavior:

- CNN-LSTM: Extracts spatial features from market indicators before processing temporal sequences.

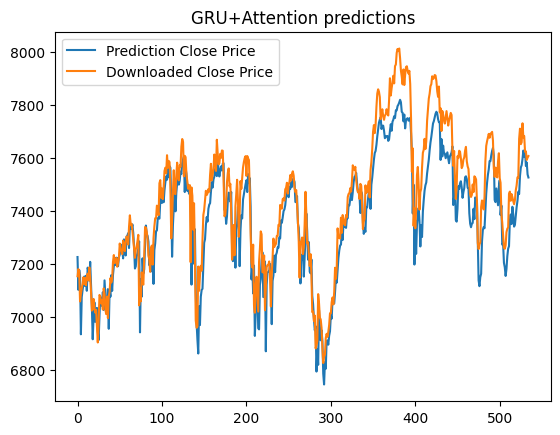

- GRU (Gated Recurrent Units): Provides efficient temporal modeling with fewer parameters, ideal for capturing mid-term trends.

- GANs (Generative Adversarial Networks): Used to model the underlying distribution of stock returns and improve robustness against noise.

- Sentiment Analysis: Integration of

vaderSentimentto process news headlines fromyfinance, providing a quantitative "market mood" feature.

Technical Stack & Implementation

Modeling

Keras, TensorFlow, Scikit-learn

Data Engineering

Pandas, NumPy, yfinance, vaderSentiment

Visualization

Matplotlib, Seaborn

Next Steps & Future Roadmap

The project is evolving from a pure forecasting tool into an integrated algorithmic trading framework.

- Advanced Sentiment Analysis: Expanding news sources beyond yfinance to include public tweets, financial blogs, and broker-specific research notes.

- Algorithmic Trading with RL: Integrating Deep Reinforcement Learning (DRL) to automate trade execution based on model predictions and risk management constraints.

- Backtesting Suite: Developing a high-fidelity backtesting engine to evaluate model performance under historical market conditions.

Interested in FinTech AI?

Let's discuss how deep learning and sentiment analysis can be applied to your financial data challenges.

Connect & Collaborate